Before I start, I gotta tell ya… I’m so stoked about the mattress giveaway we posted yesterday. We love sharing companies we love, but being able to give back in some small way to all of you for reading just takes the cake. And we have another awesome giveaway coming up next week, too, so stay tuned!

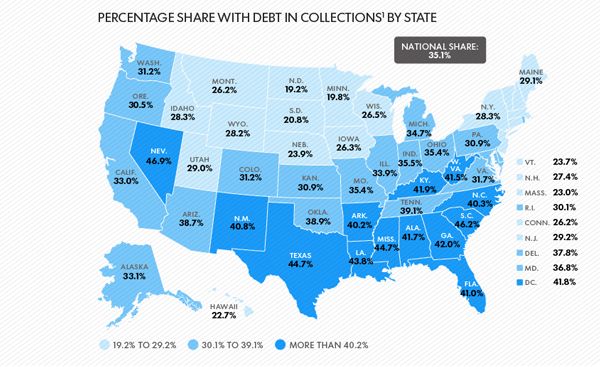

Lately, Johnny and I have stumbled across some really interesting personal finance articles. Last week, we shared the article about states’ income-happiness threshold, and we loved reading your thoughts on that topic. So I wanted to share another one today that made a splash in the news this week. A study found that 35% of Americans are delinquent on their debt payments. I wasn’t sure what “delinquent” meant (and Johnny only knew that his parents always called him a “juvenile” one). But reading the study further, it refers to having debt that’s “so far past due that the account has been closed and placed in collections … [which] … typically happens after the bill hasn’t been paid for 180 days.”

After reading the article, I didn’t really know how to react. All I know is that I just felt kind of sick to my stomach. Debt is, unfortunately, a reality that almost all of us face, but delinquent debt is happening to 35% of our country. And there are 13 states where over 40% of the population has debt in collections, including my sweet home state of Alabama.

I wish I knew how this has happened to such a significant portion of our population. Personal responsibility is certainly a factor, but I think there’s a deeper problem here. I think the real issue is a lack of financial education and awareness. The topic of debt and how to avoid it was never a conversation I remember having at home or school. I never understood how important saving was, either. And if I hadn’t married a natural saver like Johnny, I’d still probably be spending every dollar to my name.

So what happens when we aren’t taught to avoid debt, and we see those around us living with debt, and so we just assume it’s okay and live with it, and our kids will live with it, etc. Or maybe that isn’t the problem at all. Maybe the problem is entitlement and thinking we all deserve to have everything, even if we don’t really have the money to have everything. I really don’t know. But having lived under the Debt Monster’s reign for almost six years (four as a couple), it pains me to know how widespread this epidemic is.

So what’s the problem? And what’s the solution?

39 Comments

I think you’re right on the money – the problem isn’t lack of money, it’s the lack of financial education. I’m getting ready to write about it, but the jist of my thoughts on the matter are that we rely far too much on school to teach our kids – about money and everything else – rather than teaching them how to handle money responsibly ourselves. Obviously, this doesn’t go for everyone, but I feel that’s how a lot of families are.

Amen and amen. I think you hit the big, ugly nail on the head. Look forward to reading your thoughts.

I agree that financial education is lacking significantly, whether that be in the home or in schools. However, this point in the article indicates a different problem:

“At the same time, a significant number of people with debt in collections aren’t aware of the bill and may otherwise have great credit, especially when it comes to medical bills that patients often think were picked up by insurance, says Greg McBride, chief financial analyst for Bankrate.com.

“The numbers don’t necessarily speak to the percentage of households that haven’t been paying their obligations,” he says of the data.”

This gives makes me feel slightly better about the populous. Perhaps this indicates a systematic billing problem between insurers, doctors, and patients. I don’t have a solution, but perhaps this can serve as a reminder to all of us trying our best to stay on top of their debt and obligations, to do a little more digging to ensure you are in the clear.

Oooo, good eye. That didn’t jump out at me the first time I read it, but that’s a good and hope-inducing insight. Then again, later in the article it also says that these numbers don’t account for “alternative debt” like payday loans.

But regardless, wherever that true number sits, I can tell you it ain’t good. And that’s a bummer.

This actually happened to me. A Dr’s office was sending my bills to a rural physical address that isn’t a mailing address as opposed to my PO box. I didn’t realize I had 3 overdue bills until I was trying to get my law license.

The majority is most likely financial irresponsibility, but I think there may be some miscommunications here as well! Just last year I went to the dentist and was told that my insurance would cover the entire cost…and then was sent a bill. I called the dentist and was told to ignore it. This pattern continued for six months! After 6 months, the dentist said that they had made a mistake and I’d need to pay the bill. (Again, I made multiple phone calls over 6 months before they came to this conclusion). In the end, I threatened to call the BBB, so they forgave the bill, but with the way it dragged out, they could have sent it to collections. (Though everytime I called they told me that they weren’t going to do that). It was a horrible situation!

That’s a good insight. And a really good reminder… we haven’t received a dental bill from our visit back in March (!). I have no idea if insurance covered it all, but you’d think they want their money or something. We should probably get on that so that we don’t suffer a similar (or worse) fate.

I believe that it is a mixture of both a lack of education to consumers and the consumers not educating themselves, regardless if the information was provided for them or not. When I moved out on my own I worked at a mall where we had a Maurices, Express, Victoria Secret, etc. I knew nothing about debt or credit so when they offered to save me 10% by signing up for the card i figured “why not?!”. It felt like free money and living on a low, part-time income it was the perfect trap for me. I could get all of the things that I wanted without having to pay so much up front.

After racking up debt it became hard to pay and the snowball effect occurred.

I didn’t know about the ridiculously high interest rates or how not paying would affect my credit score for YEARS.

I blame myself as a consumer for not getting all of the facts before I signed on the line but I also blame a general lack of education. My parents never had the credit talk with me so i had no idea how hard you have to work to bring up your credit score and how important a credit score is. I had no idea what an interest rate really was and how it affected how much i end up paying (wasting).

In elementary school we had a class called Junior Achievement and it was about money. After that- NOTHING. I understand that the parents play a huge roll in this but I also think that schools need to educate their students about what they will be facing when they are on their own. When I was in high-school everything was aimed at going to college, they didn’t care how it was funded, they just wanted us to pick a major and a school and go. It would help if they had a class or even a seminar to discuss what they will be looking at for student loan debt based on how much they borrow or what credit card debt looks like and how all of this affects their credit and what a having a bad credit score will do to your future. The lenders will not be the ones to do it…so someone else needs to.

I look around at my peers with a mountain of debt, whether it be from credit cards they used to survive in college, student loan debt, etc. and their jobs barely pay enough to make even the monthly payments. It’s so sad.

It is definitely a broken system and it is broken at every level.

Such a great comment, Cate. Thanks for sharing. Joanna and I can totally sympathize, though. Luckily, credit card companies didn’t know where to find us when we were most vulnerable, so we avoided their preying on our lack of education.

It’s amazing to me that we could go through high school and college and never learn a thing about budgeting, credit, interest, etc. etc. I can think of 100,000 things I learned in school that are less important than those topics.

I think you and all the commenters have excellent points. Delinquent debt is probably due to a mixture of factors. I do know that once in debt it’s hard to get out without a leg up. If you don’t have resources (savings, family to lean on, a job – at all!, or good advice and good peer examples), it’s incredibly hard to dig yourself out a hole. I know many smart folks who made one wrong turn/had one stroke of bad luck in their youth (didn’t get medical insurance and had an accident, had a child with a severe disability, graduated college in 2008, etc.) and it undid them for years if not a lifetime.

I found this map that shows minimum wage by state and thought some correlation could be drawn between how much the state requires employers to pay and how much delinquent debt a resident of that state may have.

http://jewishtimes.com/wp-content/uploads/2014/02/020714_cover-story1.png

No personal draw to the paper, I just thought they had a readable graphic. Jewish Times is an interesting name for a paper!

Excellent points. And very interesting cross-reference with the minimum wage map. It’s true that debt is a wildly slippery slope. It’s easy to see how that hole gets deeper and deeper when you combine bad fortune and 15%+ interest rates. Ugh, it’s awful. I mean, I get that credit card companies and loan providers need to hedge their losses, but given the terrible circumstances many find themselves in (like the ones you mentioned), it almost seems criminal to kick people while their down like that. Maybe criminal is too harsh — extremely unsympathetic.

The major problem is almost everyone is living the same lifestyle. It doesn’t matter what you make, you have a smart phone, internet, a nice car, rent or a house payment. You go out for drinks with friends, go out to eat, go to concerts. Everyone travels and takes vacations. I have several friends with massive debt and lower incomes and they live exactly like I do. They have new big LED tvs, buy new furniture and stuff. Everyone is living the “American dream” whether they can pay for it or not. I know this is “lumping” people together, but I think you can account for 80% of the 35% this way. It is sad, but very few will live a lifestyle that matches their debt/income levels. Interesting topic.

You speak truth, Wade. It’s incredible what has become the norm for our society, regardless of one’s financial standing. Access to credit certainly exacerbates the problem. Sounds like our country needs to wake up from the American dream and start living the American reality.

I agree with all of your conclusions. Lack of education, responsibility, resources and options are all major contributors to the situation. I’m sure every person’s story is different but I know that for us, debt began out of a desire to have an education, coupled with the false notion that we needed to ‘build our credit’. That’s how we got comfortable with the idea debt (although it never actually felt comfortable). We were being told/believed that what we were doing was the financially responsible thing to do. Debt was not scary to us. But then Life (with a capital L) came along. Emergencies happened. Things snowballed. More debt was always a viable option. Until it wasn’t. I think this is how it happens for a lot of people. Nobody plans it. We were very lucky that we saw another way and pushed full steam ahead to get out of debt. We never experienced collections and paid everything off in a relatively short amount of time. Just as there are a number of contributing factors that caused the problem, there will be a number of contributing factors that solves the problem (hopefully), but I think the first step is a change in our collective cultural believe that debt is a ‘tool’ that is absolutely needed to live a financially stable life. Entitlement certainly exists, but I think it typically only comes into play when met with the normalcy of debt, the pressure to follow a certain lifestyle, and the lack of options for ‘another way’.

Very well stated. The “building credit” line is such an unhelpful diversion from what people are actually doing — borrowing money from someone else who will hunt you down until you pay them back WITH interest. I fell for the “use it as a tool” line, but luckily snapped myself out of the marketing brainwashing before my accounts were past due.

Thanks for sharing.

I agree there is a serious lack of financial education- if your parents weren’t very knowledgable about money, the odds of you getting any significant knowledge about it before the debt monster has you seem pretty slim.

That said, it’s also really easy to go to collections for medical stuff. Between figuring out what the charges are for and figuring out what your insurance should be paying and getting that resolved, 6 months goes quick. I’ve paid a $50 misc charge from a hospital that was total bullshit just to keep it from going to collections. It was an easy decision because the amount was low and my FSA had funds I needed to use anyways, but I’m sure there are plenty of people who get those sorts of unexpected medical bills for thousands instead of $50, and it’s easy to imagine that putting someone into collections.

We could do a whole month-worth of posts on how awful and confusing medical/insurance crap is. The worst. While it’s not a great alternative to straight up credit card debt, I do hope that these types of delinquencies actually account for the majority of these cases.

I wonder what the relationship is between geography and collections debt. It appears to be a spectrum from north to south, with the exception of the west coast. It’s a disheartening graphic all together. Debt is such a grind and source of stress in life, especially if there doesn’t seem to be a way out. I can’t imagine adding to that the constant harassment of collections agencies.

Yeah, that seemed pretty interesting to me. Those north-midwestern’ers seem to have things figured out. But yeah, no bueno all the way around.

Something that I found really interesting was finding out about Americans who are completely left out of the banking system, and how they play into the whole equation! I would definitely recommend watching Spent: Looking for Change, which is a documentary all about it! I’m not from the US, so some of it confused me, like not having a chequing account. You’d be hard pressed to find any 16 year old in Canada without a chequing account, so I’m not sure if there’s something that works differently there, or what, but in any case it was really interesting!

We are planning on watching it this weekend! We’ve had it on our mental queue for a long time, so thanks for reminding us. And thanks for your perspective as a non-US’er. Based on the number of Canadian PF bloggers out there, it sounds like y’all are doing something right up there. 🙂

My friends and I have talked about how we wish high school had offered a personal finance class. I took calculus, but never really learned much about how to balance a budget….which one do you think is more useful as an adult? Luckily I’m smart and could figure out how to balance a checkbook, but for many people it just doesn’t come naturally. Learning about the stock market was good (and actually really fun), but I still think a budgeting or personal finance class could have been very helpful, especially for students who weren’t planning to go to college and therefore didn’t need the calculus or other advanced math classes. Even in college it could have been helpful, just a required elective for Freshman, especially since most of us were out of the house for the first time in our lives.

Right?! Why in the world was I learning how to spin a terribly lopsided vase or how to use the restroom is Spanish/Japanese/French instead of how to pay for college? It just seems like our priorities on teaching real-world, practical subjects are wayyy messed up.

There’s definitely a lack of financial education in schools. It’s only mandatory in a handful of state’s curriculum. (I taught a personal finance class this summer that focused on budgeting, but it was an enrichment class in an affluent area – great for those kids, but what about everybody else?!) Perhaps parents don’t realize this isn’t taught in schools or maybe they don’t even know how to bring it up in their homes. Either way, the lack of knowledge is partly to blame. Just a little education on this topic would go a long way.

Amen. How did you go about teaching a personal finance class? Do you teach full-time? Volunteer? I’d be interested to see if there’s a way to offer whatever limited info we have to share to local schools in our area.

The personal finance class went really well – most of the students (middle school age) were really into SAVING a huge portion of their incomes – though they chose their own very HIGH PAYING careers. 😉 I’m a full time resource teacher during the school year and will sometimes try to slip in budgeting into my math intervention class at the end of the spring semester if I have time. As for getting finance into schools, I’m sure you could approach your local school or school district and inquire about offering a week=long finance course in conjunction with their math class. It just depends on the district and school. Good luck!

P.S. I used a budgeting course created by 21st century math projects that I purchased on teacherspayteachers.com as the foundation for my finance class. (in case you really are interested in teaching a class to students.)

Very cool! I definitely want to look into it. Thanks so much for the info.

Those numbers are truly horrifying! Like some of your other commenters, I’m hoping that at least some of it can be chalked up to issues other than inability to pay. I once had a dispute with an internet host, and the only way I could get them to cancel the account was to simply refuse to make payments. I ended up with a collection agency on me. Sorta seemed ridiculous that they would send a “debt” of $30 to a collection agency, but they did.

But in any case, I still think it’s just horrifying that debt is considered the norm these days. Perhaps this is what happens when we allow corporate interests to control the agenda.

I don’t know much about collection agencies, but they sound just as awful as the actual lenders, if not worse. I hope you made them work hard for that $30. I’d probably send them a box of $30 in pennies. With cat litter. I should stop now.

Well certainly financial education (or the lack thereof) is one of the issues related to debt but to my way of thinking it’s not the key one. Nor is it the “keeping up with the Jones” factor. Rather I see it as the lacking in responsibility, the lacking in maturity. If one looks back over the distant past, during the Great Depression, and prior to that time and even afterwards, before credit cards were invented, when cash was the only way of life, people didn’t have a lot of financial knowledge. People did however stay out of debt by first saving up the money to buy things – or simply did without – or bartered goods and/or services with their friends. There was no sense of entitlement in those days. There was no attitude of living only for today and let tomorrow take care of itself.

Sure, through misfortune, people can get into debt through no fault of their own, but I doubt that applies to the vast majority of those people making up your high debt population numbers. Just saying…

Things have definitely gotten out of hand the last 60 years or so. It’s scary how far we’ve come to accepting this new mindset of borrowing and credit.

I’d like to think education would help in instilling that level of responsibility. It can be learned, right?

I have debt in collections, and it’s not due to financial irresponsibility. It’s a medical bill. I tried to negotiate with the hospital, however they want to charge me 3x what insurance would pay. It’s very complicated and I’m now working with a lawyer. I want to pay this debt, but at a fair price. These stats don’t explain everything. I have 6 months savings and a very good understanding of my finances., but when companies don’t want to work with people there are only so many options.

Thanks so much for sharing, Randi. It’s good to know that the stats are likely significantly skewed because of situations like yours. It’s obviously lousy that you’re having to deal with it, but it sounds exactly like something we would do if we felt we were getting jerked around.

Best of luck in sticking it to the hospital-man.

I would agree that it’s due to a myriad of factors such as lack of financial education, fiscal irresponsibility, excessive medical charges and student loans. Some collections debts are due to identity theft. The victim often bears the brunt of debt that they never racked up. It can take years to clean up that mess and in the interim it negatively affects their credit.

I’m so glad you brought that up! I completely forgot that I had a speeding ticket in collections for a citation I never committed in a state I haven’t lived in for almost 10 years. It prevented me from renewing my license for almost a year (but didn’t stop me from driving, shhh). In the end, it wasn’t identity theft but just a stupid clerical error. Luckily it didn’t mess up my credit, but it took hours and hours of phone calls and months of waiting before it was resolved.

I read this post yesterday and had to think on it for awhile before answering. I think that there are several things going on. First and foremost-we aren’t paying attention to the small stuff and feel like our salaries aren’t enough for our needs. I’m specifically talking about people making the U.S. average wage which is around $50,000.

We also don’t educate ourselves or our children about money. I’m not talking investing, I’m talking about the very boring and mundane things such as savings, debt, and spending. Once we have that taken care of- everything else can happen.

Finally, we have to practice being self-sufficient and being happy with what we have. The more satisfied I am with what I have the less I’ve been spending. It’s a very surprising feeling.

Spot on. I think your second point on educating the simple stuff (savings, debt, spending) can be taught and remedied. I’m less sure about the third point of making more out of life with less. I don’t think it’s something that can be taught, at least not to the masses. I think beneath everything, this is our nation’s greatest financial threat.

I would be very curious to see these data broken down by type of debt, especially student loan and medical debt. People have been mentioning that lack of financial education in schools but I would argue that there is some financial education in schools, but it’s potentially dangerous! I know a lot of people who were told that college was the only way to a better life and higher income, so take whatever amount of loans you need to get there., even as higher education gets more and more expensive.

No one in my high school guidance counseling office ever suggested that cost should be a determining factor in choosing where to go to school. Or that it was perfectly reasonably to go to a technical school and develop a trade. The sad truth is that the ROI for college and graduate education is not what it used to be. Colleges and graduate schools tell you that will be able to pay back whatever loan you take out with your higher salary. There are even lawsuits against law schools for misrepresenting the number of their graduates who find long-term work. I’m sure there is an amount of personal irresponsibility behind these numbers, but we have to consider structural reasons behind it as well. The same is true for medical debt. People here have probably heard the oft-quoted statistic that most people who go into serious debt for healthcare costs HAVE medical insurance. That’s not right, and hopefully will be changing with the systematic changes being made in the health insurance arena.

I’m fortunate to be free of both kinds of debt, but I don’t think it’s because I’m more financially responsible.

Great points, Hallie. Usually the only guarantee a college can offer is tens of thousands of dollars in student loan debt. And while college is right for many, it’s not right for all. The cost of a school should absolutely be a major consideration for every student and parent.