Hello friends — and foes… you know who you are Mr. Panda Express guy who always scrimps on my orange chicken. There’s a special circle in Dante’s Inferno reserved just for you. Overpriced Chinese-but-not-really-Chinese food aside, I wanted to let you all in an awesome image I saw retweeted a few weeks ago.

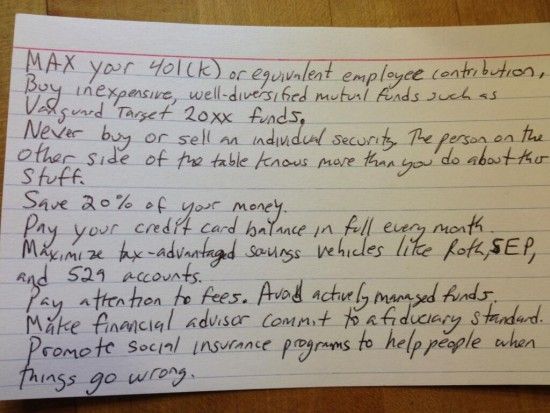

The Holy Index Card of Financial Success (tweeted by @m_sendhil)

The Holy Index Card of Financial Success (tweeted by @m_sendhil)

Those who know me well know that I’m a sucker for financial tips. And I’ve actually always been obsessed with notecards. In college, I amassed hundreds of chicken-scratched 3″ x 5″‘s with questions and key terms on one side and answers and definitions on the other. Joanna would probably define my studying methods as “neurotic,” but we’ll just pretend that’s a compliment. At any rate, this notecard image was right up my alley.

There’s not much of a backstory to the image, but it’s important to know its author: University of Chicago professor Harold Pollack. A finance teacher he is not (health policy is his expertise), but Harvard/Princeton/Yale PhD he is. Needless to say, dude’s smart. And beyond smart, he knows how to distill a mountain of financial guidelines, best practices, and opinions into a notecard of 10 simple tips. Here’s my brief analysis:

- Max your 401(k) or equivalent employee contribution.

Yes, yes, YES! Remember folks — it’s free mon-ay! If you need a refresher on why you should jump on this bandwagon, here’s where we’ve made that case before. - Buy inexpensive, well-diversified mutual funds such as Vanguard Target 20xx funds.

If you’re not familiar with Target funds, they’re actually incredibly intuitive. Say you’ll be 65 years old in 2050. If you invest in a Target 2050 fund, the fund will auto-magically adjust over time from investing more aggressively (lots of stocks) to more conservatively (lots of bonds). And while most Target funds have the same purpose, their fees (what you’re paying the people managing the mutual fund) vary wildly. Vanguard is known for having some of the lowest fees, which means more money goes in your pocket instead of theirs. - Never buy or sell an individual security.

This is another way of saying, “diversify.” I’ve made this mistake and I won’t make it again. There will likely be some naysayers out there, but if you’re a noob to investing, heed this advice. - The person on the other side of the table knows more than you do about this stuff.

“I hear what you’re saying and note your concerns, but I’m going to go with my gut and trust that random commercial I saw during daytime TV that told me to cash out all of my investments and buy gold.” - Save 20% of your money.

I’m not sure where he came up with this number, but a guess would be the 70-20-10 rule: 70% living expenses, 20% savings, 10% debt. There’s also Elizabeth Warren’s 50-30-20 rule which allocates 50% to wants, 30% to needs, and 20% to savings. I’m not a huge fan of that method, but in any event 20% seems like a great benchmark. - Pay your credit card balance off in full every month.

Duh. If you can’t follow this one, no more credit cards for you. Here’s our take on credit cards. - Maximize tax-advantaged savings vehicles like Roth, SEP, and 529 accounts.

The more money you put toward these weird-sounding acronyms, the less Uncle Sam will hold you accountable when you pay your taxes. And that’s always a good thing. - Pay attention to fees. Avoid actively managed funds.

As mentioned in #2, fees eat away at your investment earnings. Any time you’re researching mutual funds, look at the Gross Expense Ratio. Let’s say Mutual Fund XYZ has a 1.75% expense ratio. That doesn’t seem too high, right? Well, let’s say your mutual fund earns 7%. That would mean 25% of your earnings would be lost to fees. That’s a lot of dough. That doesn’t mean that high fees always equate to poor funds, but be cautious of unseen costs that will eat at your earnings. - Make financial advisor commit to fiduciary standard.

Fiduciary is such a weird word. Fi-do-she-airy. Fiduciary. Weird. Anyway, it’s a weird word that has a simple meaning: acting in your best interest. That means your financial profits should come before theirs. Seems like that’s what every financial advisor should do anyway, but that’s just not the case. - Promote social insurance programs to help people when things go wrong.

Sure, I guess. I do my part in “promoting” those programs every time I look at my paycheck and realize a whole lot of it is missing. 🙂 Beyond your involuntary responsibilities to support public programs, helping individuals and charities is a great place to put extra money.

While there’s probably more that goes into financial success, this is as good a starting list as I’ve ever seen. That being said, I’m sure we’ll have differing opinions on a few of these items. So what do y’all think? Any kool-aid on this notecard that you aren’t drinking?

19 Comments

I would replace number 5 with “save the highest possible % of money”. Why limit it to 20% if you can save more. We are currently above 50% (whilst still paying the mortgage on our primary property).

Otherwise, its a darn good list for a beginner to personal finance.

Agreed. I think 20% is a nice starting place, but if you can afford to save more, that number shouldn’t hold you back.

And kudos to you guys! That’s an awesome saving rate.

Not a bad set of rules. This person doesn’t seem to be following the most aggressive path toward financial independence (aka early retirement), however. For that I would make some modifications:

1. Contribute enough to get the full employer match (if any). After that, consider saving in an account that you will be able to tap without penalty before you turn 59.5 years old.

2. Good idea for the 401k or other long-term retirement savings accounts.

3. Read up on strategies for investing in individual securities (like the endless list of Dividend Growth blogs/websites) before investing this way. But given the right strategy, buying and holding individual securities can be even lower-cost in the long run than buying the investments recommended in point #2 above.

4. This may or may not be true, especially after you’ve done much studying in preparation for point #3. The person on the other side of the trade may be investing for the very short term, whereas you are likely to be investing for the long run. So you are trading based on different objectives. This could be mutually beneficial to both parties involved in the transaction.

5. Save at least 20% of your money. There is no reason you couldn’t aim for 35%, or 50%, or 70%. The more you save and invest, the faster you reach FI.

6. Hard to improve on this one.

7. Whenever you put money into an account with restrictions on future withdrawals, you’re giving up freedom on how you can use that money. Make sure the restrictions are offset by some benefit (tax advantage, etc) which helps you toward your goal.

8. Make sure the cost of any investment matches the benefit you gain from any investment. As stated before, even low-cost index funds are more expensive in the long run than an individual security bought once and held for years.

9. Do you need a financial advisor? Is the benefit gained from this worth the cost?

10. This is more of a political question, but one could argue that an ounce of prevention is worth a pound of cure.

The note card is a great idea!

In response to “Executioner” (what a foreboding name!):

I think point 3 and 4 are supposed to go together. Unless you are a financial expert, chances are the person on the other side of the table DOES know more than you. I mean… this is a Harvard/Yale/Princeton guy telling us that he even looks to experts in this field. Yes, do your homework, AND seek out excellent advisors.

8. Great point.

9. I know I do! Between my husband and me, we have a house, 2 separate 401k plans, an IRA, 2 separate employer insurance (life/health/disability, etc) plans, 2 separate outside life insurance plans and some outside stocks/bonds/inheritance that are a lot to understand and manage. We want to make sure we’re covered, that our money is really working hard for us and that we have a good retirement plan in place. We want it individualized so we sought out an expert!

10. Agreed, it’s political. Whether you are of the “pick yourself up by your own bootstraps” type or the “redistribution” type, having opportunity for upward mobility at all levels benefits everyone. I imagine that without opportunity, we’d live in a world that’s a cross between South Africa (huge crime because of income inequality) and Atlas Shrugged (huge defection due to unfairness). I hope that makes sense and doesn’t sound like I’m taking a side. I can see both points of view here!

Thanks for noticing my work.

best

HAP

Thanks for stopping by, Professor! And moreover, thanks for making sense of all the mumbo jumbo out there and focusing on tried and true principles.

Seems like some solid advice. Unlike the above commenters, I think 20% is totally appropriate! Not everyone is aiming to live meagerly and retire early :).

I giggled at the “I do my part in “promoting” those programs every time I look at my paycheck and realize a whole lot of it is missing.” Very true!

“Live meagerly and retire early.” Amen. A nice idea in theory, but I’d rather not always live for tomorrow.

How neat! I also loved notecards in college. I always put terms and definitions on them and had people quiz me. Sadly I still have some notecards left and have no clue what to do with them, but I will find something! I agree with the words on the notecard and your supporting comments – I think it’s a great standard guide for the average person. Of course, other people will want to be more aggressive, but for normal people who don’t nerd out on personal finance, I think it’s a must-read.

Haha. I think I have some rubberband-ed stacks of notecards lying around, too. That is, the ones that Joanna hasn’t found and thrown away yet. 🙂

It’s crazy to see that a prudent financial plan can exist on a small note card. People need to block out the “noise” of the financial networks/publications, find a strategy that fits their comfort level, and stick to that plan.

Whenever we sit with 401(k) participants, it’s crazy to hear some of the nonsense that comes out of their mouths. Simple is effective, efficient, and easy.

– Mark

Effective, efficient, easy. I’m a sucker for alliteration, so I’ll likely use the three E’s in the future. Thanks, Mark.

Vanguard has come to Canada and I have already purchased a small amount of shares of a high dividend ETF. I have been paying too much for a bank run mutual fund in my RRSP (registered retirement savings plan) and I have an appointment next week to dump it (it is worth more than I have in it) and buy more Vanguard ETFs.

I hope someone listens to the “save 20%” portion of your post. I didn’t and it will be a long time until I retire and I will have to scrimp and save for years until I have enough to retire.

Vanguard is great. High ratings, low fees. Glad to hear you’re making the switch and hopefully saving a lot on fees.

Financial success may be an awesome term for many people. However, it entails determination and rational thinking to attain this target. Thanks for your suggestions. These are very good points that can be useful for many persons.

Awesome list. I pretty much agree with all 10. Looks like your old health policy professor really knew his stuff.

Tip 3, Never buy or sell an individual security,really hit home for me. I had a family member who lost close to $10,000 of his savings almost overnight because he invested it in an individual security that tanked. Needless to say, his financial tragedy taught me this lesson.

Tip 5, Save 20% of your money is also an awesome guideline too. I personally go by the 70-10-10-10 rule, which is 70% towards living expenses, 10% towards passive capital (i.e. savings), 10% active capital (investing in businesses, real estate etc.), and the last 10% for giving to the greater good( kind of similar to your 1oth tip).

All in all, great financial tips. I am sure any person who took these tips and applied them would be setting themselves up for success. Thanks for sharing.

Nate

It sounds like you’ve learned a lot and are making some smart financial choices, Nathan. I relaly like you 70-10-10-10 rule. That’s a great way to approach money!

Great tips, even though some are specific to the USA ( I’m based in Sweden)

I should research equivalents for some of the investment programs you suggest though!

I must say, I’m super uninformed on other countries’ investment programs, but from what I’ve heard from fellow non-USA’ers, most countries have very similar programs.

The Internet still amazes me sometimes — not only do we have so much information available at our fingertips, but that we can share tips and chat with folks from all over the world. So cool.